Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

This article is an on-site version of our Unhedged newsletter. Premium subscribers can sign up here to get the newsletter delivered every weekday. Standard subscribers can upgrade to Premium here, or explore all FT newsletters

Good morning. Alphabet reported after the close yesterday, and management said the company would double its capital spending in 2026, to about $180bn — a mind-boggling figure that blew past expectations. That the stock only fell less than two per cent in late trading after this bombshell dropped felt like a positive sign after an unsettling day (about which more below). Email us: unhedged@ft.com.

Not just tech and not just this week

The S&P 500 is down just 1.3 per cent over the past two days, but it doesn’t seem like it. It feels instead like the market is a washing machine set to the spin cycle.

The change in the index has been modest because, while there have been big moves all over, they have mostly offset one another. Since Monday’s close, 79 of the S&P’s components have fallen 5 per cent or more, and 93 have risen 5 per cent or more. The biggest stocks have been hit hard; of the Magnificent Seven, only Apple has risen. The equal-weight S&P 500 is actually up.

Nominally, what is happening is a tech sell-off sparked, first, by the possibility that AI tools may make some traditional business software companies uncompetitive and, second, by weak earnings reports from chipmakers Qualcomm and AMD. But what is happening is much bigger than just tech and indeed has been happening for longer than just two days. The market is undergoing a structural shift.

As Yin Luo of Wolfe Research pointed out to me, we have seen a reversal in which “factors” — broad characteristics that drive stocks’ returns — are leading the market. He sent me the below screenshot of his factor dashboard from yesterday, showing that stocks with high dividend yields, low valuations and high return on equity did well yesterday, while momentum, high volatility and growth all got smacked down.

Investors’ love affairs with growth, risk, and doubling down on whatever has been working are over. Previously unpopular, low-growth, defensive stocks are on top. The big winners this week have included such wildly unsexy names as Old Dominion Freight Line (trucking), International Paper (packaging) and Brown-Forman (booze).

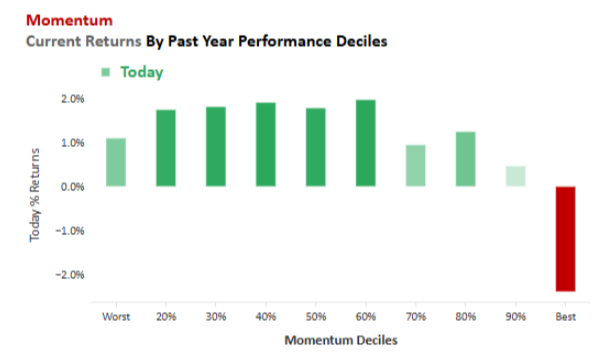

The violence with which the leaders of the old regime are being thrust aside is highlighted by Nomura’s Charlie McElligott, who sorted stocks into performance deciles for the past year, and then showed the performance of those deciles in yesterday’s trading. The first truly were last:

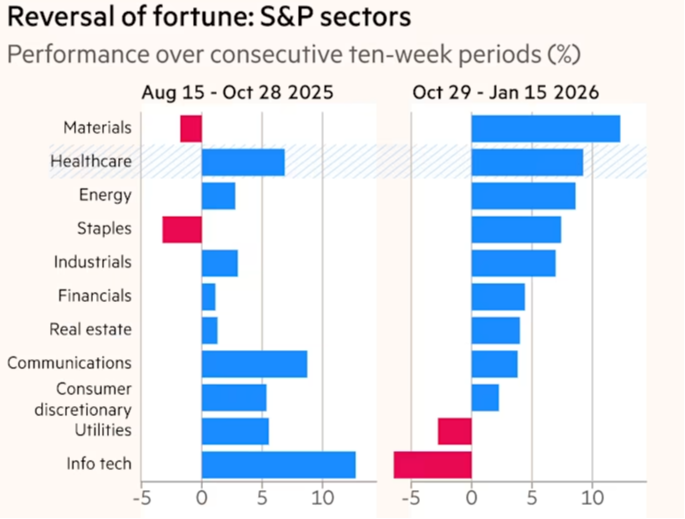

This is not a phenomenon of the past few days, either. The shift began at the end of October, as we pointed out in our chart of the week a few weeks ago. We illustrated the point then in terms of a flip-flop in sectoral leadership, a reversal that has only accelerated recently:

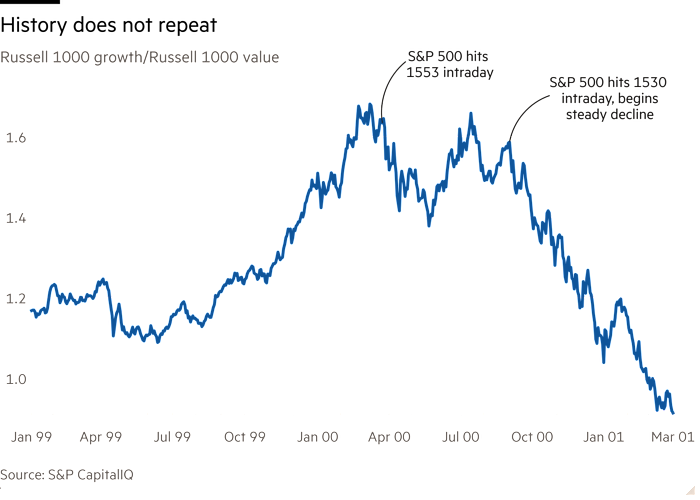

What does all this portend? One ominous idea making the rounds yesterday is that the current shift in leadership resembles the one that occurred in 2000, a few months ahead of the dotcom market crash. That ugly episode can be captured by looking at the relative performance of growth and value indices. Growth had been crushing value in the second half of 1999, but started to falter in February 2000, a month before the wider market peaked in March, and long before the broad market started falling hard in September. In this chart, a rising line shows growth outperforming value:

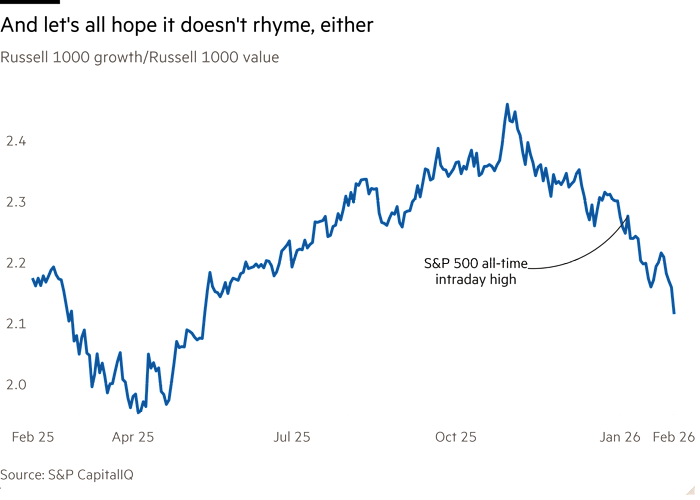

Here is how the relative performance of growth and value look now:

The AI boom is very different from the dotcom boom in that it is led by big, profitable companies, not hopes and dreams. So a return-to-rationality crash is less of a risk today. Still, the later stages of two periods have in common a sense that universal optimism about an agreed narrative is giving way to uncertainty, debate and apprehension. This suggests the near future will bring sustained volatility at best and at worst a meaningful correction.

(Armstrong)

Readers on the sentiment puzzle

In Tuesday’s letter, we asked how to reconcile the divergence between dismal “soft” measures of consumer sentiment and strong “hard” measures of spending and output. A lot of readers wrote in to share their views.

One reader, a quant and former academic, wrote to argue that the sentiment surveys are just not very good indicators:

Whenever I see macroeconomists try to glean messages from associations between aggregate variables I shudder a bit, and more so when a variable is an aggregated average of elicited survey responses [about] a subjective ‘expectation’

Fair enough, but there is clearly a feeling of discontent and worry out there, and it would be useful to know where it is coming from. One point made by other readers was that market gains don’t make much of a difference to the many Americans without security portfolios, explaining part of the divergence in sentiment and why consumption has risen faster than disposable household income. John Authers of Bloomberg, who also recently took a stab at the topic, put it in terms of the familiar metaphor of the “K-shaped economy”:

The people on the top bar of the K are helping to drive a cyclical rebound with the profits they have made. The equity tail . . . may be wagging the equity dog.

But by far the most common reader response was that poor sentiment reflects fear of being professionally displaced by AI. A software engineer wrote:

Through the 2010s it felt as though I had strong job security and would be forever in demand; this ended with the post-2021 tech job market crash. Compounding this, AI coding models seem to have made a step-change improvement during the past few months, changing the game. Despite being happily employed, I now feel as though if I look away for a month, my job role might totally change (or vanish). Transferable skills I’ve spent years cultivating could be worthless. I’m sure this realisation has been hitting other knowledge workers too . . . ‘It’s AI, stupid,’ feels like a facile answer, but may be a big piece of the puzzle for folks like me who arrogantly thought we’d always be indispensable.

The research on when AI will meaningfully impact employment and productivity, and by how much, is so far inconclusive. Most studies estimate the impact won’t fully take place until at least a decade. But if you write code, drive a truck, diagnose illnesses or write about markets, the sound of the career clock ticking is getting louder.

(Kim)

One good read

An interesting life.

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.

Recommended newsletters for you

Due Diligence — Top stories from the world of corporate finance. Sign up here

The AI Shift — John Burn-Murdoch and Sarah O’Connor dive into how AI is transforming the world of work. Sign up here